The Uniform CPA exam is a standardized exam comprising of four parts that all CPA license applicants in all states and jurisdictions are required to pass with at least 75% each, regardless of the other state-specific requirements. If they fail to do so, they will not qualify to apply for CPA licensure. These must all be passed within an 18-month window, or the first section passed will expire when that timeframe is exceeded. These four parts are FAR, REG, BEC and AUD.

The Regulation (REG) part of the exam focuses on testing the examinees knowledge and skills regarding US tax accounting, specifically in relation to federal taxation, ethics and responsibilities to tax practice and business law.

The REG exam is broken into two parts, each worth 50% of the exam. The first part consists of 76 multiple choice questions, while the second consists of 8 task-based simulations (TBS). The purpose of these questions is to assess your ability to remember and understand information, to apply the information that you have learned and your analytical skills. These are split over 5 segments:

REG is a four-hour long examination.

The best study method for anything thing is subjective, as each person has their own learning styles that work best for them. However, one of the most important study methods that most CPAs recommend is to at least aspect is to practice doing as many multiple-choice questions (MCQs) as you can. There are many free MCQs available online, as well as paid ones. While doing them, you should take notes when you get the answers wrong and then review that content again later. Many people feel that waiting a couple of days and then trying again until you get 90-100% for the set is a good approach. After that, you can move onto the next set. This approach will help you to strengthen your weaker knowledge areas, while also helping you to familiarize yourself with the type of questions that are likely to appear in the exam.

Additionally, it is a good idea to set a manageable study schedule for yourself with breaks and rewards to recharge yourself with. You should also make use of the resources that are available to you, such as the study plans and guides by Becker’s and Wiley, if you can afford it, or even some of the other cheaper and free study told that are available. Although just going through the material is helpful, a good way to really internalize it is to summarize the notes as you go along and make to also make index cards of the important definition or topics with which to revise later. If you have time, even read through the notes and cards as soon as you have finished compiling them, so that it sinks in more. Another benefit to summarizing the chapters of your chosen workbook, is that it forces you to engage with the information and to wrap your head around the concepts, instead of just reading them through. If there is a particular section that you are struggling with, then give it a break and go back to it. You could also then try a different approach, such as watching a lecture on it, such as those of Farhat’s Accounting Lectures and Edspira.

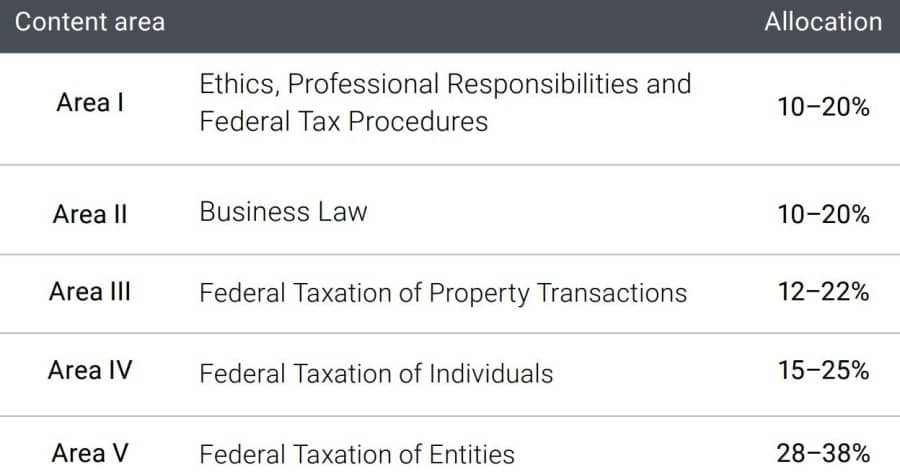

The purpose of the REG exam section is to assess the applicant’s skills in terms of evaluating and analyzing the given information, applying their knowledge of accounting techniques to the concepts, as well as their remembrance and comprehension of that knowledge. The exam covers five content Areas, which in turn, cover a variety of subtopics. This is shown below.

According to the AICPA’s CPA exam Blueprint effective from July 2021, the subjects are covered as follows:

The amount of time that you should dedicate to Regulation (REG) is really dependent on your familiarity with taxation laws, but the AIS-CPA suggests dedicating between 90-110 hours towards studying for this part. If you work in tax, you may be able to get away with studying 3-4 hours a day over a 3-week period, if you are able to fit in the time. If not, and especially if you struggled with taxation during college, then 6-7 weeks with 2-3 hours a day might be better. This is because it will give you time to slowly process and internalize the concepts, as opposed to trying to cram in as much as possible a quickly as possible while risking forgetting things or getting confused during the exam.

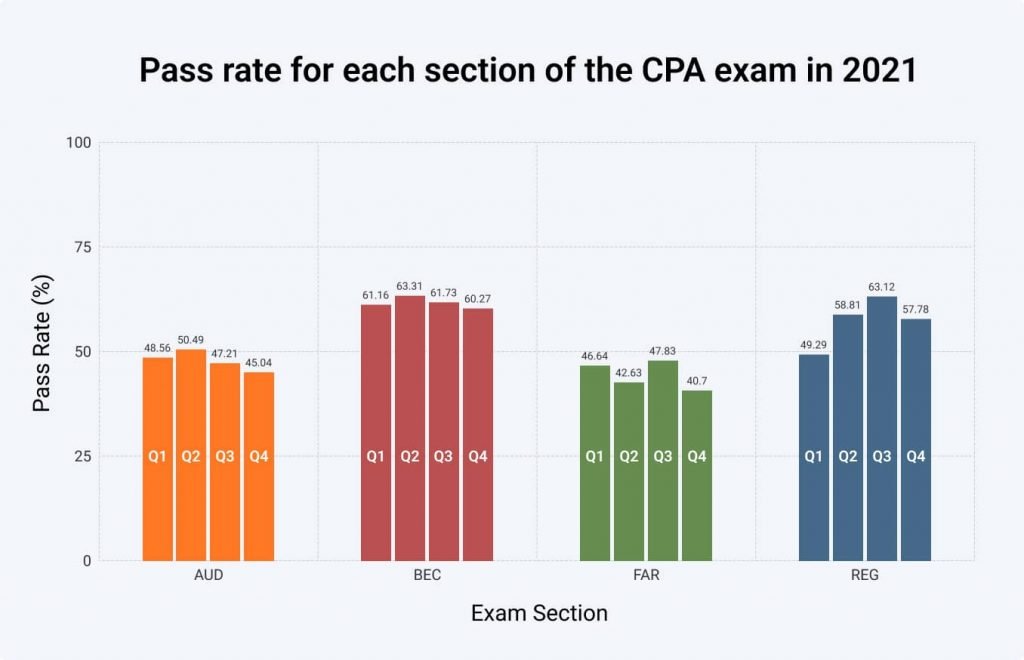

With a pass rate of only around 60%, the REG part is far from easy. However, it is still considered to be easier than both the FAR and AUD parts of the exam. It should be easier for those applicants who chose to fulfill their experience requirements in a public accounting firm. As there is only an 18-month window in which all four parts of the Uniform CPA exam should be passed, or the earliest pass will expire. This is why many candidates choose to take the harder sections first, since they have the highest rate of failure.

There are many guides and resources available to help you study for the REG exam. Some of these are online, while others are available in hardcopy, and there are also some that are free and others that are premium. Some examples are:

News and information

News and information Refund Policy

Refund Policy Firm Partnerships

Firm Partnerships CPA Requirements by State

CPA Requirements by State FAQ

FAQ